Pet Insurance Cost: Key Factors That Influence Monthly Premiums

Pricing Mechanics: Deductibles, Reimbursement Rates, and Benefit Limits

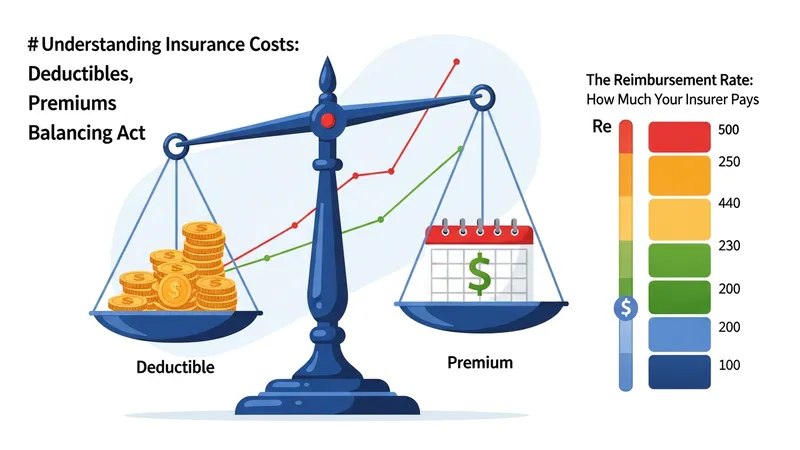

Deductible choices are a primary tool to manage monthly premiums; selecting a higher deductible typically reduces an insurer’s expected per-claim outflow and may correspond to lower monthly payments. Deductibles can be structured annually or per-incident, and that framing changes the owner’s exposure profile. Insurers price each structure differently because per-incident deductibles may lead to smaller claims being processed more often, altering administrative cost expectations and potentially affecting premiums.

Reimbursement rates determine the share of eligible costs an insurer will cover after the deductible is applied. Typical reimbursement tiers may range broadly (for example, lower to higher percentage bands), and higher reimbursement percentages are associated with higher monthly premiums because the insurer expects to bear a larger portion of approved claim costs. The interplay between deductible level and reimbursement percentage shapes both monthly premium and expected out-of-pocket exposure when a claim occurs.

Benefit limits—including annual, per-condition, or lifetime maximums—affect pricing by capping insurer liability over defined periods. Policies with generous or unlimited benefit frameworks generally require higher monthly contributions because they leave the insurer open to ongoing high-cost claims. Conversely, time-limited or per-incident maximums reduce the long-term claim exposure and may be reflected in lower monthly rates. Evaluating these limits helps clarify trade-offs between premium level and potential long-term financial coverage.

Policy renewal practices and indexed pricing clauses also influence ongoing monthly costs. Some insurers adjust premiums over time based on claims experience, pet age, or broader cost inflation in veterinary care; these mechanisms may lead to stepwise changes in monthly payments at renewal. Transparency in how renewals are calculated contributes to clearer expectations about future monthly costs, and understanding typical renewal drivers can be an important consideration when comparing long-term premium trajectories.