Cash Now Pay Later Loans: Understanding How Short-Term Financing Works

Types and structures of cash-forward short-term financing

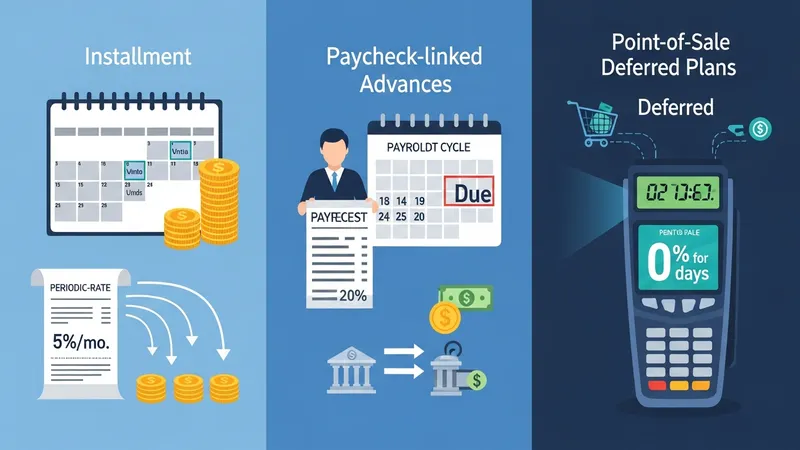

Short-term cash-forward financing comes in multiple structural forms that may suit different purchase contexts or timing needs. Installment advances divide repayment into a set number of scheduled payments and often include a finance charge expressed as a periodic rate or a flat fee. Paycheck-linked advances connect repayment to payroll cycles and can reduce the need for frequent transfers but may concentrate liability on a single date. Point-of-sale deferred plans can be interest-free for brief promotional periods or carry fees that activate if the balance is not cleared within the promotion window. Each structure typically prioritizes speed and convenience over duration.

Providers choose structures that balance underwriting burden with customer access. Minimal-document offers may approve small advances rapidly based on automated checks, while products that offer larger amounts typically require more documentation. Promotional point-of-sale options are often integrated into merchant checkout processes and may rely on third-party underwriting platforms. From a consumer perspective, understanding whether the product is a true installment obligation or a deferred single-payment obligation clarifies the timing of principal reduction versus fee accumulation.

Common features across structures include automated repayment initiation, options for early repayment, and specified consequences for missed payments. Automated transfers reduce operational friction but require confirmation of payment sources and calendar alignment; users may find that scheduling conflicts with bank holds or payroll timing can cause inadvertent misses. Early repayment options often reduce future interest accrual, but some contracts include prepayment fees or do not adjust flat fees, so contract terms should indicate whether early payoff materially changes the total amount due.

When evaluating these structures, a practical consideration is how typical use cases align with household cash flow cycles. Short-term advances may fit short timing gaps between expenses and incoming funds but can also create concentrated repayment obligations that intersect with other periodic bills. Modeling several repayment timelines can reveal stress points where multiple obligations coincide. These alignment considerations are often as consequential as headline pricing when assessing practicality.