Cash Now Pay Later Loans: Understanding How Short-Term Financing Works

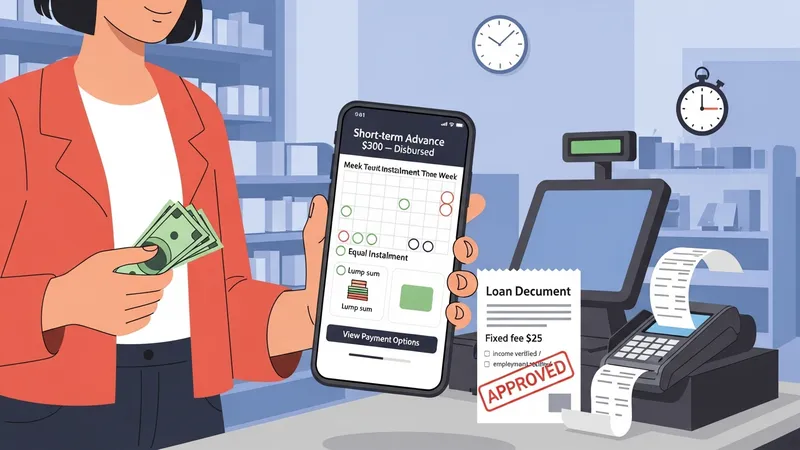

Short-term financing that delivers cash up front with scheduled repayment over weeks to months is a category of consumer credit characterized by rapid disbursement and condensed repayment timelines. These arrangements generally provide small principal amounts relative to traditional personal loans, and they often combine a fixed fee or short-term interest with defined installment or lump-sum repayment. Lenders or platforms that offer this format may assess income, employment stability, or account activity quickly to support faster decisions than many longer-term lending products.

Such near-term credit structures can be offered at point of sale, through mobile platforms, or by specialist lenders. They can differ from revolving credit in that the obligation is typically a one-time advance with a finite repayment schedule rather than an ongoing credit line. Consumers and analysts commonly distinguish these products by factors such as origination speed, fee structure, whether installments are equal or graduated, and whether early repayment changes total cost.

- Short-term installment loan — A single disbursement repaid in several scheduled installments over a few weeks to several months; cost elements often include an interest rate or fixed fees.

- Paycheck advance or earned-wage access — Advances against expected earnings repaid from the next paycheck or via scheduled deductions; availability can be tied to employer payroll cycles.

- Point-of-sale deferred payment plan — Financing initiated at purchase that delays full repayment or splits payments over a short period; terms can vary between interest-free promotions and plans with fees if not repaid on schedule.

When comparing these example structures, it is useful to consider how approval criteria and processing times may differ. Point-of-sale deferred payment plans often require minimal underwriting and can be approved in real time, while some installment products may use more detailed income verification and can take longer to fund. Fee disclosure, short-term annual percentage rate (APR) equivalent, and repossession or collection policies for missed payments are variables that may vary by provider and by jurisdiction. Consumers and researchers often examine sample repayment scenarios to understand effective costs across formats.

Repayment scheduling patterns typically fall into two general groups: equal periodic installments and backloaded or balloon-style payments. Equal installments split principal and any interest or fees into recurring payments due weekly, biweekly, or monthly, which can aid predictable budgeting. Backloaded schedules may reduce near-term outflows but often increase total cost exposure if interest accrues. For payroll-linked advances, repayment alignment with pay dates may reduce short-term strain but can concentrate outflows on the next pay period, which is an operational consideration for household cash flow modeling.

Cost components for these short-term advances often include explicit finance charges, origination fees, or flat service fees, and may be expressed as APRs or as per-transaction fees. Fees that appear modest in absolute terms can translate into high short-term APR equivalents when the term is brief, so it is common to compare both nominal charges and their time-adjusted impacts. Providers may also charge late or returned-payment fees that increase the total amount due if scheduled payments are missed; these secondary charges are relevant to risk assessment and planning.

Risk and consumer protection aspects vary by jurisdiction and provider type. Regulatory frameworks in many areas impose disclosure requirements, caps on certain fee types, or rules on collection practices, and those frameworks can affect both product design and cost. Credit reporting, eligibility impacts, and the presence or absence of hardship or dispute-resolution processes are additional considerations that may influence longer-term financial outcomes. Analysts often recommend reviewing contractual terms and hypothetical repayment scenarios to evaluate potential exposures.

In summary, immediate-disbursement short-term advances are a diverse set of credit arrangements that combine quick funding with compact repayment schedules. Differences in underwriting, fee structure, repayment mechanics, and regulatory treatment mean that comparable headline charges can have different practical implications for cash flow. The next sections examine practical components and considerations in more detail.