Quick Books: Managing Invoices, Bills, And Everyday Bookkeeping Tasks

Quick Books: Managing Invoices, Bills, and Everyday Bookkeeping Tasks — Invoicing and Client Billing

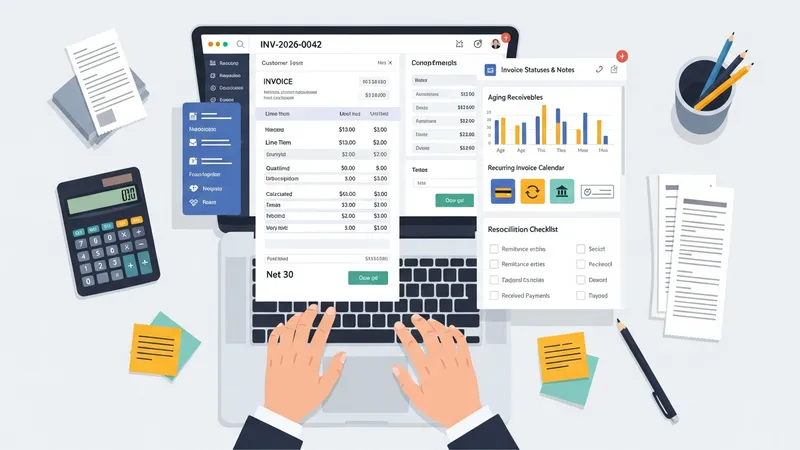

Invoice workflows typically begin with creating an invoice record that includes customer details, line-item descriptions, unit prices, taxes, and payment terms. Many systems allow for customizable templates so documents match organizational naming conventions and information requirements. Businesses often set standard payment terms such as net 30 or net 45, and they may track aging to monitor outstanding receivables. For repeat services, recurring invoices may be scheduled, which can reduce repetitive entry while still requiring periodic review to confirm accuracy.

Payment processing options linked to invoices often include electronic payments, bank transfers, and checks. When electronic payment integrations are used, remittance information should be reconciled to received transactions to ensure payments are applied to the correct invoices. A clear invoice numbering system helps prevent duplication and supports an audit trail. Invoice statuses and notes provide visibility into customer interactions and can be used to document agreed adjustments or credits.

Tracking accounts receivable requires regular review of aging reports that summarize unpaid invoices by period (current, 30, 60, 90+ days). Aging reports may be used for internal cash-flow planning and to inform collection communications. Some organizations implement standard follow-up sequences; others prefer case-by-case handling based on customer history. Balancing the need for timely collections with customer relationships typically requires calibrated communication and documented payment arrangements when needed.

When invoice disputes or credits occur, documenting adjustments formally and issuing credit memos maintains clarity for both parties and preserves a clear ledger history. Applying credits and refunds should be recorded in the accounting system with references to the original invoice. Consistent practices for handling discounts, early-payment terms, and write-offs reduce ambiguity in financial statements and simplify reconciliation during closing periods.