Accounting Services: Streamlining Payroll, Invoicing, And Expense Tracking

Invoicing practices tied to financial recordkeeping

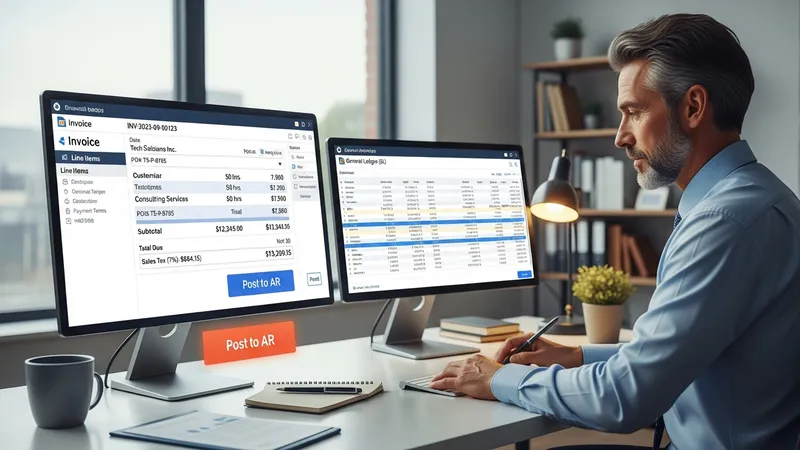

Invoicing practices shape revenue recognition and accounts receivable balances when integrated with accounting systems. Common invoicing elements include standardized invoice numbering, terms of sale, tax treatment, and linkage to sales orders or contracts. Organizations may adopt electronic invoicing or maintain paper invoices; the principal accounting requirement is that each invoice be traceable to a sale and mapped to revenue accounts in a way that supports periodic financial reporting.

Integration of invoicing with the ledger can be direct or indirect. Direct integration posts invoice transactions to accounts receivable and revenue accounts automatically, while indirect processes may rely on a billing system that periodically exports invoices for posting. Each choice may affect month‑end workload and reconciliation; for example, batch exports may require verification of totals and sequence checks to ensure completeness of posted invoices.

Controls for invoicing typically focus on authorization, customer credit checks, and matching processes where applicable. Matching invoice lines to shipping documents or service confirmations can help validate that revenue is recognized appropriately. Aging analyses and accounts receivable reports often serve as internal controls to monitor collection performance and to identify invoices that may need dispute resolution or collection follow-up.

Invoicing also interacts with tax reporting and regulatory obligations in many jurisdictions. Proper tax categorization on invoices and retention of invoice copies can aid in preparing tax filings and responding to inquiries. When invoices span multiple accounting periods or include credits and adjustments, clear documentation and supporting schedules are commonly used to explain how such items were treated in financial statements.